A buyer’s guide to financing a new home build

Financing a new home build works differently from purchasing an established property. Instead of a single loan settlement, construction projects usually involve staged payments, land purchases and lender approvals tied to building contracts.

For buyers comparing builders, house and land packages or custom designs, understanding how the finance process works early can make the planning phase significantly smoother. Many buyers now begin this process by exploring their borrowing capacity through digital mortgage platforms such as LendUs, which allow them to assess loan options while still researching land and builders.

Rather than waiting until plans are finalised, buyers can explore borrowing capacity and loan options at the same time they begin researching land and builders.

How construction loans differ from standard home loans

The biggest difference between building and buying is how funds are released.

With an established home purchase, the loan is typically drawn down in one transaction at settlement. Construction loans, however, are released in stages as the build progresses, from slab or base stage through to completion.

At each stage, the lender releases funds directly to the builder after confirming that construction has progressed according to the contract. Because lenders assess the building contract, plans and builder details before approving the loan, finance decisions can influence which builders or construction arrangements are viable.

Explore your borrowing power with LendUs

The right home, the right loan

Traditionally, comparing home loans involved meetings with banks or mortgage brokers and multiple rounds of paperwork. Increasingly, you can explore loan options online during the early research phase of a build.

Digital mortgage platforms analyse financial information and compare loan products across multiple lenders, helping you understand what may be achievable before committing to a builder or design.

Many platforms allow you to:

Estimate borrowing capacity within minutes

Compare loan products across multiple lenders

Upload financial documents securely online

Track application progress digitally

If you are juggling builder comparisons, land searches and design decisions, these tools can simplify the finance side of the process.

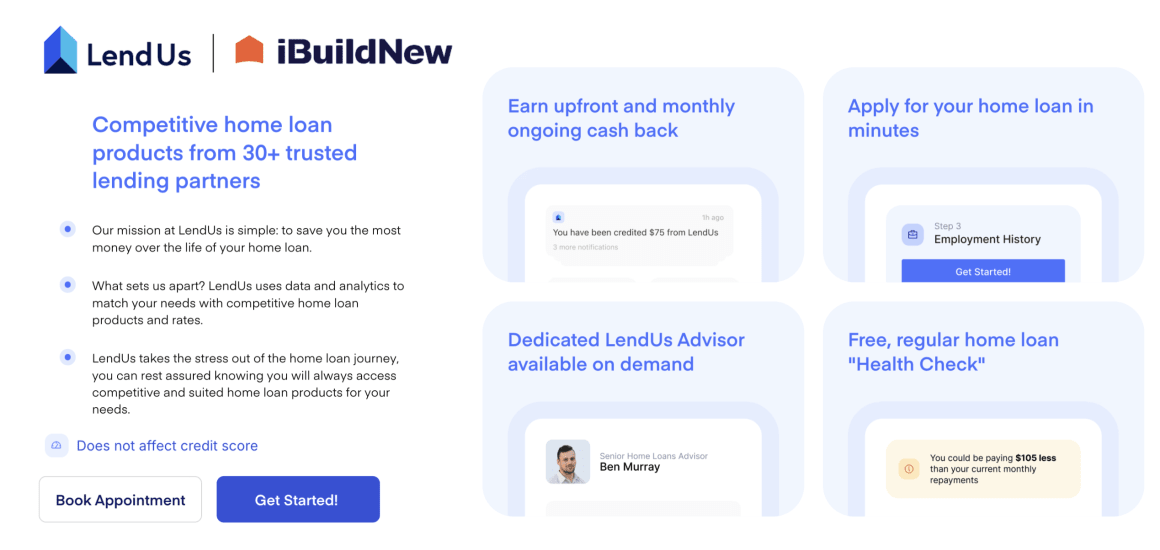

Platforms such as LendUs, a digital home loan broker, use digital tools to assess borrowing capacity in minutes, match borrowers with loan products across a panel of lenders and streamline documentation through a simplified application process.

LendUs provides access to more than 30 lenders, allowing buyers to compare a range of home loan products suited to different financial circumstances. Borrowers are also paired with a dedicated home loan adviser who can guide them through the process, from early qualification through to settlement.

Some of the features available through the platform include:

Real-time borrowing insights

Buyers can receive an estimate of their borrowing power within minutes. This helps establish a working budget before engaging builders or signing construction contracts.

Access to a wide lender panel

Rather than comparing banks individually, borrowers can review loan products from more than 30 lenders, offering greater visibility across rates, structures and lending policies.

Dedicated loan guidance

A home loan adviser supports borrowers throughout the process, assisting with documentation and guiding applications through approval.

Cashback incentives

Eligible borrowers may also receive cashback benefits, including an upfront payment and ongoing monthly cashback linked to their loan.

Finance your build with LendUs’ exclusive cashback offer

How to estimate borrowing power before choosing a builder

Before committing to a builder or signing a building contract, it helps to understand how much you can borrow and what repayments may look like.

Estimating borrowing power involves assessing several financial factors, including your income, existing debts, living expenses and available deposit. Lenders use these details to determine how comfortably you could manage repayments over time.

For example, lenders typically review:

employment income and job stability

current debts such as car loans, credit cards or personal loans

regular household expenses

savings history and deposit size

These factors are used to calculate your serviceability, which ultimately determines how much you can borrow.

For construction loans, lenders also assess the total cost of the project, which usually includes the land purchase price, the builder’s contract price and any estimated site costs. This combined figure becomes the total loan amount being assessed against your financial capacity.

Understanding this early can help you move more confidently when the right block of land or house and land package becomes available.

A clear borrowing estimate can help you:

Narrow down suitable builders and home designs

Set realistic budgets for upgrades or inclusions

Move quickly when land releases become available

Avoid redesigning plans later to meet lending limits

Finance options for different buyer types

Once you understand your borrowing capacity, the next step is identifying the type of loan structure that suits your circumstances.

While the fundamentals of borrowing remain similar, finance needs can vary depending on your situation.

If you are a first home buyer, you may need guidance navigating grants, deposit requirements and lender eligibility rules. If you are upgrading or downsizing, you may need to balance the sale of your existing home with the timing of a new build. Investors typically focus on loan structures that support long-term property strategies.

If you are self-employed, lenders may require additional documentation to demonstrate income stability. Some homeowners also explore refinancing options to reduce repayments or release equity to fund a new project.

How to prepare for a construction loan application

Regardless of which lender or broker you use, preparing financial documentation early can help streamline the loan approval process.

Lenders typically request:

Recent payslips or income statements

Tax returns or financial statements for self-employed borrowers

Details of existing debts and financial commitments

Evidence of savings or deposit funds

Information about the land or property you are purchasing

Once you select a builder, lenders will also review the building contract, plans and progress payment schedule before issuing formal construction loan approval.

Starting the finance process early

If you are still in the early planning stages, exploring finance options can provide useful context before engaging with builders or signing a building contract.

Understanding borrowing capacity and loan structures helps frame the decisions that follow, from the type of home design that fits within your budget to the suburbs or estates that remain financially realistic.

Digital finance platforms allow you to begin this process online, offering an early snapshot of borrowing capacity and loan options before the building journey fully begins.

Click here to explore your borrowing options and get started with LendUs

iBuildNew Editorial Team

As the specialist voice of Australia’s largest new home building resource, the iBuildNew Editorial Team delivers deep-dive coverage into the house and land sector. From analysing new estate launches to highlighting the country’s leading home designs, we track the building journey to provide clarity for every buyer.