Melbourne land market strengthens as buyer confidence returns

Melbourne’s housing market is showing signs of steady recovery, with confidence building across both established and greenfield segments.

In accordance with Cotality, established housing supply remains around 20 per cent below average, maintaining upward pressure on prices as sellers gradually return to the market. Affordability remains tight, limiting price growth to a forecast 5–6 per cent over the coming year.

Auction clearance rates have lifted to 73 per cent, the highest in a month, supported by the 5 per cent Deposit Scheme and stronger buyer sentiment ahead of the Melbourne Cup weekend.

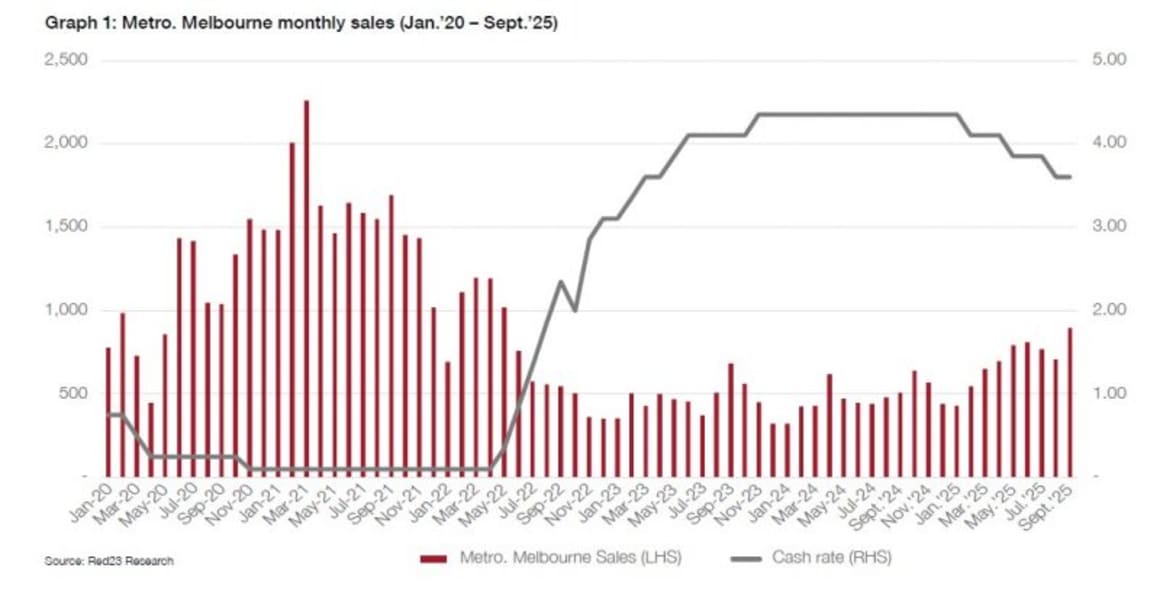

The land market continues to improve, recording 890 sales in September and a quarterly average of 780 per month across the year. Greater Geelong remains a standout, achieving 120 monthly sales. Melbourne has recorded 6,300 land sales year to date and is on track to reach 8,500–9,000 sales in 2025, the strongest result in two years.

Land availability continues to tighten, with 33 per cent of available lots currently titled, unchanged since August 2024.

Greater Geelong has also seen a notable boost in sales, with more than 150 transactions recorded in September, the highest since February 2022, capturing 15 per cent market share when combined with Metro Melbourne results.

Wyndham and Casey continue to dominate Melbourne’s land sales, contributing 25 per cent and 24 per cent of total transactions respectively. Both growth corridors remain highly sought after due to extensive land supply and competitive pricing. Hume and Melton each accounted for 14 per cent of monthly sales, supported by steady activity across established estates. Whittlesea captured 10 per cent, driven by consistent sales in Wollert, while Cardinia (8 per cent) and Mitchell Shire (5 per cent) maintained stable performance.

Melbourne’s median land price rose modestly by 0.5 per cent in September to $418,000, marking the third consecutive month of stable performance. While overall growth remains subdued, buyer confidence and steady sales volumes are supporting gradual improvement.

Greater Geelong has also seen a notable boost in sales, with more than 150 transactions recorded in September, the highest since February 2022, capturing 15 per cent market share when combined with Metro Melbourne results.

Wyndham and Casey continue to dominate Melbourne’s land sales, contributing 25 per cent and 24 per cent of total transactions respectively. Both growth corridors remain highly sought after due to extensive land supply and competitive pricing. Hume and Melton each accounted for 14 per cent of monthly sales, supported by steady activity across established estates. Whittlesea captured 10 per cent, driven by consistent sales in Wollert, while Cardinia (8 per cent) and Mitchell Shire (5 per cent) maintained stable performance.

Melbourne’s median land price rose modestly by 0.5 per cent in September to $418,000, marking the third consecutive month of stable performance. While overall growth remains subdued, buyer confidence and steady sales volumes are supporting gradual improvement.

Among municipalities, Casey led growth with a 3.5 per cent month-on-month rise to $503,000, followed by Greater Geelong (+2.4 per cent), Hume (+1.5 per cent), and Melton (+1.0 per cent). These areas benefited from stronger sales momentum and limited titled stock. In contrast, Cardinia (-0.9 per cent), Whittlesea (-0.7 per cent), and Mitchell (-1.5 per cent) recorded mild declines due to softer release activity and selective price adjustments.

On an annual basis, Hume (+7.4 per cent) and Casey (+7.0 per cent) have recorded the strongest year-on-year gains, reflecting sustained demand across Melbourne’s northern and southeastern corridors. Wyndham (+3.0 per cent), Whittlesea (+2.8 per cent), and Greater Geelong (+1.1 per cent) also posted annual growth, while Cardinia (-1.9 per cent) and Melton (-2.2 per cent) remain slightly below 2024 levels.

Overall, land values across Metropolitan Melbourne remain resilient, supported by consistent demand and constrained new supply. The market continues to stabilise, establishing a firm foundation for gradual price growth through late 2025 and early 2026.

Among municipalities, Casey led growth with a 3.5 per cent month-on-month rise to $503,000, followed by Greater Geelong (+2.4 per cent), Hume (+1.5 per cent), and Melton (+1.0 per cent). These areas benefited from stronger sales momentum and limited titled stock. In contrast, Cardinia (-0.9 per cent), Whittlesea (-0.7 per cent), and Mitchell (-1.5 per cent) recorded mild declines due to softer release activity and selective price adjustments.

On an annual basis, Hume (+7.4 per cent) and Casey (+7.0 per cent) have recorded the strongest year-on-year gains, reflecting sustained demand across Melbourne’s northern and southeastern corridors. Wyndham (+3.0 per cent), Whittlesea (+2.8 per cent), and Greater Geelong (+1.1 per cent) also posted annual growth, while Cardinia (-1.9 per cent) and Melton (-2.2 per cent) remain slightly below 2024 levels.

Overall, land values across Metropolitan Melbourne remain resilient, supported by consistent demand and constrained new supply. The market continues to stabilise, establishing a firm foundation for gradual price growth through late 2025 and early 2026.

Greater Geelong has also seen a notable boost in sales, with more than 150 transactions recorded in September, the highest since February 2022, capturing 15 per cent market share when combined with Metro Melbourne results.

Wyndham and Casey continue to dominate Melbourne’s land sales, contributing 25 per cent and 24 per cent of total transactions respectively. Both growth corridors remain highly sought after due to extensive land supply and competitive pricing. Hume and Melton each accounted for 14 per cent of monthly sales, supported by steady activity across established estates. Whittlesea captured 10 per cent, driven by consistent sales in Wollert, while Cardinia (8 per cent) and Mitchell Shire (5 per cent) maintained stable performance.

Melbourne’s median land price rose modestly by 0.5 per cent in September to $418,000, marking the third consecutive month of stable performance. While overall growth remains subdued, buyer confidence and steady sales volumes are supporting gradual improvement.

Among municipalities, Casey led growth with a 3.5 per cent month-on-month rise to $503,000, followed by Greater Geelong (+2.4 per cent), Hume (+1.5 per cent), and Melton (+1.0 per cent). These areas benefited from stronger sales momentum and limited titled stock. In contrast, Cardinia (-0.9 per cent), Whittlesea (-0.7 per cent), and Mitchell (-1.5 per cent) recorded mild declines due to softer release activity and selective price adjustments.

On an annual basis, Hume (+7.4 per cent) and Casey (+7.0 per cent) have recorded the strongest year-on-year gains, reflecting sustained demand across Melbourne’s northern and southeastern corridors. Wyndham (+3.0 per cent), Whittlesea (+2.8 per cent), and Greater Geelong (+1.1 per cent) also posted annual growth, while Cardinia (-1.9 per cent) and Melton (-2.2 per cent) remain slightly below 2024 levels.

Overall, land values across Metropolitan Melbourne remain resilient, supported by consistent demand and constrained new supply. The market continues to stabilise, establishing a firm foundation for gradual price growth through late 2025 and early 2026.iBuildNew Editorial Team

As the specialist voice of Australia’s largest new home building resource, the iBuildNew Editorial Team delivers deep-dive coverage into the house and land sector. From analysing new estate launches to highlighting the country’s leading home designs, we track the building journey to provide clarity for every buyer.