First Home Buyers: Here’s How You Could Buy With Just A 5% Deposit

Following the federal election promises back in May, the Government has now provided more details around the First Home Loan Deposit Scheme that aims to support eligible first home buyers to enter the property market and purchase their first home faster. The Coalition Government unveiled the latest...

Following the federal election promises back in May, the Government has now provided more details around the First Home Loan Deposit Scheme that aims to support eligible first home buyers to enter the property market and purchase their first home faster.The Coalition Government unveiled the latest details of its scheme, confirming the number of applicants will be capped at 10,000 each year at a first-in best-dressed basis. Buyers taking out their first home loan will be able to gain finance with a deposit as little as 5%, with the government acting as the guarantor for the remaining 15%. The scheme is expected to commence on 1 January 2020 and will be administered by the NHFIC.

So how does it work?

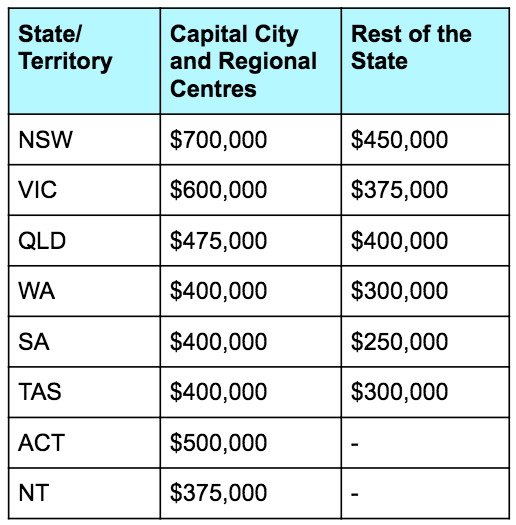

First home buyers will need to meet a number of eligibility criteria in order to have access to this scheme. As mentioned above, this scheme will offer up to 10,000 loans each financial year to eligible participants. Singles who earn a taxable income of $125,000 per year or under will be able to access the scheme. Couples who have a combined income of $200,000 per year will also be eligible.First home buyers will have to prove they have never owned a home before in Australia. They will also need to be an Australian Citizen and at least 18 years of age. Although the government is being the guarantor for the remaining 15% of the loan, first home buyers still have to eventually pay it back. Even though your lender will still do their normal checks on your financial situation, this makes it easier to get a loan without having saved for a full 20% deposit.The scheme also revealed the price thresholds set out for every capital city and larger regional centres across the country which have a population greater than 250,000 people. This includes places such as Geelong, Illawarra (Wollongong), the Sunshine Coast, Gold Coast and Newcastle and Lake Macquarie. These were set according to local property market prices and conditions and to help even the playing field across the country.

What are the risks involved?

Since the amount left owing is obviously going to be larger, there is a risk in taking out a loan with a smaller deposit, resulting in your mortgage lasting longer than it otherwise would. The standard maximum loan term is 30 years and your mortgage will not likely extend beyond this. But, if you take out a larger loan over the same loan term, your minimum repayments will also need to be larger. This means the mortgage taken out under the 5% deposit scheme could actually put more pressure on borrowers to pay it back, and their month to month cash flows.Another risk or consideration involved with this scheme is that borrowers will have to pay more total interest over the course of the loan. Because the deposit will be smaller, the amount against which your interest will be calculated will be bigger than someone with a full 20% deposit, although in a low-interest-rate environment this should be manageable for most.Why is the government doing this?

This scheme is a part of a promise given by Scott Morrison during his election campaign in May. Also, having more first home buyers who are able to service their own loans means we have a stronger and more balanced economy. However, giving 10,000 first home buyers a year access to quick deposits could actually push up the prices of more affordable properties, which is something we have seen over the years with increases to first home buyer grants. Nonetheless, the scheme is ultimately there to help young Australians get into the property market sooner than they otherwise may be able.How can I apply for this scheme?

The scheme will be administered by the NHFIC and applications will need to go through this institution. Although applications have not yet opened, the NHFIC will provide further details on the procedure, eligibility assessment and regional price caps closer to the start date of 1st January 2020.Whatever you are looking for in a new home, make sure to speak to our independent consultants. They are here to help you 7 days a week and assist you with all of your queries regarding the new home building process or even investment opportunities. Call them on 1800 184 284, online.iBuildNew Editorial Team

As the specialist voice of Australia’s largest new home building resource, the iBuildNew Editorial Team delivers deep-dive coverage into the house and land sector. From analysing new estate launches to highlighting the country’s leading home designs, we track the building journey to provide clarity for every buyer.